You may have seen in the news that we have seen a fair bit of volatility in the UK government bond market (and therefore the equity market) this week, with UK 10-year government bond yields rising to their highest rate since 2008, leaving the UK Chancellor in a difficult position following on from the Autumn budget. In our market commentaries, we have highlighted how the bond market reacted negatively to the announcements made in the budget, with concerns about inflation and growth largely dominating the news headlines in the months that followed. This week, we saw lower demand for longer dated UK government bonds in a key bond auction, indicating a lack of faith in Reeves’ plans to deliver the growth needed to finance the national debt. As a result, with investors needing higher rates to justify the higher level of risk premium the market sees in these assets, yields increased and the currency weakened, having a knock-on effect on UK investors’ portfolios.

Is This Only A UK Story?

At the same time as yields have increased on UK bonds this week, we have also observed a sharp upward movement in US government bond yields, as markets speculate over the potential Trump tariffs we expect to be announced later this month, alongside data indicating persistent inflation and a strong labour market in the US, which are feeding into expectations for interest rates to remain higher for longer. We would like to reiterate that this is a very different situation to the UK economy, which is showing signs of weakening confidence and economic activity, therefore requiring more interest rate cuts to stimulate growth. That being said, bond markets do tend to be influenced by US movements, with US inflationary concerns feeding into UK yield movements.

Why Are Yields Now Rising?

When we look at the movements we have seen this week, the rise in government bond yields looks to be an overshooting of the recalibration of interest rate expectations and fiscal policy speculation that has been taking place since before the US election. It has been characterised by pricing a lower probability of rate cuts from the US Federal Reserve and the Bank of England and steeper yield curves (higher yields for longer dated bonds). We view this as an overreaction within markets, which we see as a temporary move which will reverse as reality sets in and interest rates fall.

Why Are We Seeing Weakness in Equities?

As fixed income yields rise, we are also seeing weakness in equity markets. With valuations appearing stretched following strong equity market performance, particularly in the US, the rises in yields could create a rotation out of equities into fixed income, although it is too early to say that this is happening just yet. The S&P 500 is currently 2.8% below the 6th December high, however we could see a further step down should bond yields continue to rise.

Are You Making Any Changes To The Portfolios?

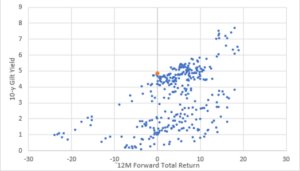

While this week’s movements can be unsettling, we would advise investors to keep calm and ignore the short-term noise in markets, and therefore we are not looking to make any changes to the portfolios at this time. Based on the last 30 years, yields at these levels have been bond buying opportunities. Looking at UK gilts, forward-looking 12-month total returns have always been positive when the 10-yr yield has been above 4.7% (current 4.84%). This is shown in Chart 1 below.

We are seeing the highest UK Gilt yields since 2008. These are rare entry points for fixed income and reflect that upside inflation and fiscal risks have already impacted on pricing. As a result, if we did not already own these assets, this would be a buying opportunity because they are extremely attractive. That does not go to say that yields cannot increase further, however we must consider the outlook for these assets moving past the noise and irrationality currently being seen, and the outlook is positive.

Chart 1: Gilt Yields and Total Returns (1997-2024)

Source: AXA Investment Managers, 10/01/2025

Overall, while it can be concerning to see negative movements in markets and the short-term impact it can have on portfolios, it is key to remember that this is a short-term move driven by sentiment and speculation, and our outlook remains unchanged and positive for 2025.

If you have any questions, don’t hesitate to get in touch.

Past performance cannot be used as a guide to future performance and the value of your investment will fall as well as rise in value. You may not get back all of your investment and the final value of your investment will depend on the performance of your portfolio. The actual performance of an individual client’s portfolio may differ due to different funds being used and being restricted in relation to certain asset allocations. Performance figures quoted include fund manager charges but exclude adviser, discretionary, custodian and switch charges. Unless stated, income is reinvested into the portfolio. The information contained in in this document is for information purposes only. It does not constitute advice or a recommendation or an offer or solicitation for investment.